Once upon a time there was a country — it had its problems as any nation does, but it did well enough. Its people prided themselves on working hard, and they were comparatively well off: less so than the UK, more so than Spain and Italy.

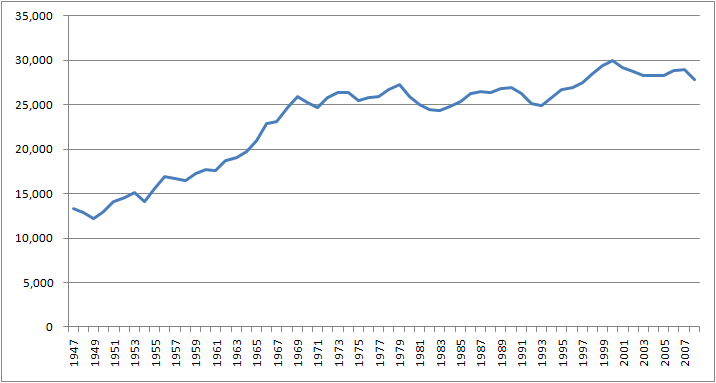

They’d had the good fortune to have none of their infrastructure destroyed during World War II, and after the war they experienced a boom as an exporter. Things slowed, however, in the late 60s and early 70s. Some said this was because the rest of the world got better at growing their own food and manufacturing their own goods. Others said it was because they allowed too much immigration. Some said it was because the welfare programs they created in the 60s ate away at the motivation to work hard. Others said it was because unions became weak. Whatever the reason, their average income in inflation adjusted terms grew much more slowly than it had, and there was a good deal of discontentment and disagreement as to what to do about it all and who was at fault. Here’s a graph of their average family income in inflation-adjusted US Dollars.

Now, many of you may already see quite clearly what I’m playing at. This country is ours — to be precise it’s part of ours. The graph above is a graph of the income of the 20th percentile of US families in constant dollar terms (inflation adjusted to 2008 dollars). And if you want to see why it is that people get angry about the graph, one need only add a second trend, the income of the 80th percentile of US families:

When you put these two next to each other, what gains the 20th percentile has seen look pretty paltry. For whatever reason, the people who inhabit the 80th percentile in regards to earnings are doing much better in terms of increasing their income than those in the 20th percentile.

There are plenty of theories as to why this could be: immigration, technology, less unionization, welfare, low taxes, businesses being eeeeeeevilllllll, etc.

One of the things I’ve been wondering about lately is whether the global marketplace affects different segments of the US population very differently. I was trying to think of a way to look for this, and what I came up with was looking at the percentage of the world GDP which is represented by the US GDP. Unfortunately, the data source I found for this (the World Bank, see sources below) only had data since 1960, which is unfortunate because the theory I wanted to look at was this:

The US emerged from WW2 as the premier industrial power, and the only first rank power without significant damage to its infrastructure from the war. Thus, the whole world was one big market for American goods (manufactured, agricultural, etc.) in the period right after the war and up through the 60s. However, as the rest of the world recovered/developed, working class Americans increasingly experienced competition from abroad. However, because the the continued global dominance of the US, more skilled and educated US workers continued to reap the benefits of overall world economic growth.

This struck me as interesting, in that at a visual level it did seem to show that back when the income of the 20th percentile was growing rapidly in the 60s, the US made up a larger percentage of World GDP, and yet the rest of the world was growing rapidly. That would seem to fit with a story my story very roughly. It also seems interesting that the US percent of world GDP stablizes right around the time that the 20th percentile’s income hit its plataeu, around 1970.

I’d need data going back to 1947 and a better way of representing the degree to which the US was the engine of global post-war economic growth. I’d also need to come up with some clearer idea of what changed around 1970.

So I don’t think there’s a clear conclusion here, but I thought the visuals were at least interesting enough to share.

SOURCES

US income data: http://www.census.gov/hhes/chroot/home/ae6ff503/the-american-catholic.com/html/income/data/historical/inequality/f01AR.xls

World economic data: http://data.worldbank.org/indicator/NY.GDP.MKTP.CD?cid=GPD_29

You might want to add something else to your little graph there. In the 1950s, the highest nominal tax rate (the tax rate that would have affected the 80th percentile, but not the 20th) was 90%. It has fallen significantly as supply side economics and other such silliness were applied, and today, that same tax rate is a little less than 40%. Apparently, allowing the rich to keep their money and stash it in the Cayman Islands isn’t as good for the US GDP as conservatives might think.

PF,

Actually, the top marginal income tax rates didn’t affect the 80th percentile either. For instance, in 1950, income over 200k was taxed at 90%. This data, however, is inflation adjusted to 2008. If you inflation adjust 200k in 1950 to 2008, it’s $1.7 million. However, the 80th percentile of income was only $41k (in 2008 dollars). If you adjust that back to 1950 dollars this is $4,600 which would put you in the 26% tax bracket for 1950.

Interesting question though.

Historical tax tables:

http://www.taxfoundation.org/publications/show/151.html

Inflation calculator:

http://www.coinnews.net/tools/cpi-inflation-calculator/

Exactly right, Darwin. Leaving aside the rather obvious noxiousness of a 90% income tax rate, that rate actually hit very few families. Inflation adjusted, income tax rates are higher today for virtually all high income earners, which is not to say that this somehow provides a contrary explanation for the phenomenon you describe — that is doubtful. But facts will never dissuade class warriors. Their personal failures are always the fault of someone more successful — you can count on it.

Another partial explanation for the phenomenon described in the graphs is the sexual revolution, which increased both ends of the income spectrum. High income households include many two-income professionals (something pretty rare until the late 1970s) — doctors don’t marrry plumbers. And low income households are disproportionately composed of a single female with children, a very costly and very modern phenomenon.

Another related observation: inflation adjusted income statistics do a very imperfect job of actually describing changes in standard of living, which changes are actually quite pronounced for households at every level. Even households at the 20% level live in much better conditions than the modest inflation adjusted income increase would suggest. More own homes; both apartments and homes are larger and usually have air conditioning; computers, televisions, microwaves, mobile phones, etc. are plentiful; and a much greater percentage of low-income families own cars. Even food is much cheaper (inflation adjusted) with unbelievably greater variety. Moreover, the percentage of meals the average member of a 20% household eats outside his own home would be unimaginable to that person’s counterpart in 1950.

You need to be careful with this sort of information to verify what is being measured and what is being excluded. Some data series fail to take into account fringe benefits, or measure only wages and not salaries, or exclude the value of government benefits like Medicaid. Variation over time in the size of households is often not accounted for either. I have heard also criticisms of the Census Bureau as a producer of economic statistics (not its core mission). The Bureau of Economic Analysis or the Bureau of Labor Statistics might be a better bet.

allowing the rich to keep their money and stash it in the Cayman Islands isn’t as good for the US GDP as conservatives might think.

1. How many people are doing that?

2. Of what do the loan portfolios of banks domiciled in the Caymen Islands consist?

AD,

I predict you will not receive a helpful answer. The facts, I’m afraid, are not compatible with the class warfare narrative. More self-affirming to ignore them and continue on in smug moral superiority, however delusional.

“There are plenty of theories as to why this could be: immigration, technology, less unionization, welfare, low taxes, businesses being eeeeeeevilllllll, etc.”

Because labor and capital are disunited. That is the fundamental reason. Nearly 40% of the stocks in this country are owned by the top 1% of income earners. The next 40% is owned by the next 9%. The bottom 90% owns about 20%. And there is a similar story with respect to business equity, financial securities, trusts, non-home real-estate – everything related to investment.

Large incomes are derived from ownership of property. Small incomes are derived from wages. Every CEO has a salary, but it is a minuscule fraction of his income when set against dividends. Thomas Montag, the “global banking and markets” executive at Bank of America, had an income in 2009 of over 29 million dollars.

Only 600,000 of that, or a little less than 3% was in salary. 97% of that 29 million was derived entirely from stock awards. Now this is an extreme case, but on average the compensation of CEOs, as I’ve seen, breaks down in similar ways – most of their income is derived from stocks, and comparatively little from salaries.

These are simple facts, not cries of envy or to redistribute the wealth. Narrowing the income gap means narrowing the property gap.

Joe, the income and property gap distinction is not that elegant. The stock grants to CEO’s for instance is all wage income as a practical matter. It is true that the truly super rich earn most of their income from investments, but most high income earners do not. The pattern is disarmingly common. People work for compensation for many years in order to build wealth that will eventually allow them to generate most of their income from invested assets. CEOs are no exception. Warren Buffett counter-examples are pretty rare. Somewhat more common are those who inherit wealth, though they normally do a pretty good job of diluting and dissapating it over a few generations.

I can see the attraction in trying to unite labor and capital via ESOPS etc, but there are potentially serious pitfalls. It is normally imprudent to place most or all eggs in one investment basket, which is what entrepreneurs and small businessmen are willing to do — and they make up most of the wealthy in this country (which does not remotely mean most of them achieve wealth). The willingness to take risk and the ability to successfully manage it through entrepreneurial skill is not equally shared among all workers. Most people are better off accumulating wealth through long-term diversified investments substantially disassociated with their workplace.

on average the compensation of CEOs, as I’ve seen, breaks down in similar ways – most of their income is derived from stocks, and comparatively little from salaries.

I believe this is largely a function of the minutia of the tax code, which taxes compensation at a higher rate if it comes from stock than if it comes as salary.

If someone is employed at a publicly traded company, nothing prevents him from immediately converting as much of his wages as he wishes into company stock. If he converts it all to stock, this is functionally equivalent to what he would have gotten in compensation if he had been paid in stock in the first place. That so few people do this suggests that they prefer being paid in wages (you might say that this is just inertia, but suppose for a moment that Bank of America decided to start paying its employees with stock; if this happened, my guess is that a) the employees would not be happy about it, and b) upon receiving their stock they would immediately convert all or most of it to cash).

BA,

Yes, the reason CEO comp is stock heavy is simply because boards want CEO comp tied to company fortunes and there are some tax advantages in doing so. There is an intuitive appeal to ensuring that CEOs pay is tied to investor fortunes, but it does have some perverse consequences including an emphasis on short-term thinking as well as the potential for huge comp packages beyond what may be intended or anticipated. Many public company boards struggle with this.

A good analysis, but I think that the reason for our relative decline starting in the early 70’s comes from the fact that our tax and regulatory system became increasingly hostile to wealth creation. And it was the big corporations, big government and big unions who wanted it this way – it protected established wealth and power.

A genuinely free market means a continual and rapid over turn of the socio-economic elite. This sort of thing is not desired by those at the top – and, so, they’ve made it harder and harder for anyone to do anything which might create sufficient new wealth to allow entry in to the upper reaches of society. The only people who have been able to continue rising are those in entertainment and sports (you might want to consider that while baseball stars and movie idols were popular 70 years ago, they didn’t for the most part hob nob with the elite…that is something which only happened when such persons started raking in the many millions of dollars necessary to purchase entry).

Getting back on track really involves no more (and no less) than breaking the chains on the economy. Just allow people to work as they will, and things will go back to the old, American norm.