NEW: Massive line forms outside Silicon Valley Bank in California as customers panic.

Welcome to Biden’s America. It will only get worse.pic.twitter.com/MNCQuKIc9h

— Collin Rugg (@CollinRugg) March 10, 2023

Jim Cramer said Silicon Valley Bank was a buy last month at $320

Today it is being closed by California regulators pic.twitter.com/x1xMBTrQTS

— Inverse Cramer (Not Jim Cramer) (@CramerTracker) March 10, 2023

Tucker Carlson and Stephanie Pomboy break down the Silicon Valley Bank debacle:

"We are on the brink of a 2008-style financial crisis, and I'm not trying to be hyperbolic." pic.twitter.com/027puArugp

— The Post Millennial (@TPostMillennial) March 11, 2023

Economies are frequently like engines. They give off signs when the system is in distress. The collapse of the piggy bank for Silicon Valley may be indicating another 2008 if we are lucky, another 1929 if we are not. Fear not, the Biden administration is on the job to tell us that this can be cured with more diversity and more equity.

EXCLUSIVE‼️

Footage from inside the Silicon Valley Bank pic.twitter.com/CfEKtHMA9p

— Zhao DaShuai 无条件爱国🇨🇳 (@zhao_dashuai) March 11, 2023

Corruption and insider trading. Ask Biden, he’s perfected the art. Hope the common folks get their money out of there.

Yesterday, as always, FDIC put out a press release on subject.

I’m pretty sure that due to the reactions to the Wuhan flu, for nearly three years, the bank was not subjected to an on-site CA/FDIC bank examination. Just saying.

Mac, I love Stephanie Pomboy. She’s loaded with data. And she’s brilliant. And she sings that song every week on Maria Bartoromo Fox Business for the past 15 years. That being said, she’s always worth a listen.

This was a boutique/niche [a very large one] lender that got caught in the necessary Fed reactions to the boom caused by Biden’s insane spending and the Fed’s money printing. On that level, this may be symptomatic of a systemic ‘issue.’ The next ‘shoes to drop’ likely would be insolvencies of fin. institutions concentrated in commercial real estate and consumer loans. It’s something to watch.

Per my much-smarter brother, Cramer’s stock advice is almost as bad as NYT/Princeton Paul Krugman’s economic analysis/predictions.

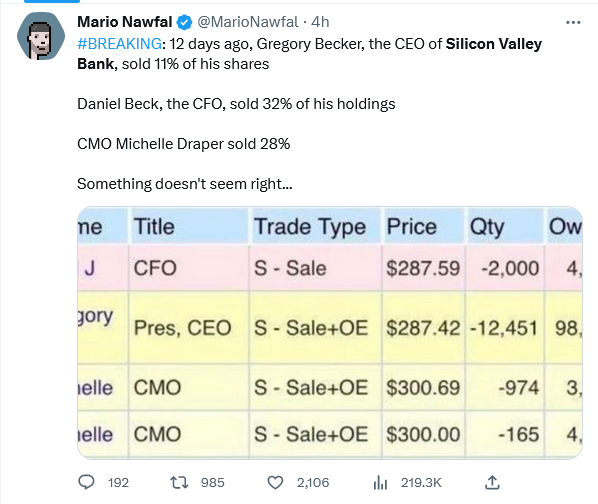

A few weeks back, the Insiders/rats were deserting [selling shares] a sinking ship.

I was in this business for a while during the 1980’s Ag/oil financial crisis and S&L crisis. Some pundits are saying it failed because it couldn’t sell $2.25 billion in new stock – they try that befier every bank bankruptcy. That’s only the tip of the viceberg [pun intended].

The root cause seems too many defaulted loans among the tech start-ups – the vast majority of the bank’s borrowers.

Of the $175 billion in deposits, about $150 billion were over the $250,000 FDIC insured amount. Ergo, [on Fox Business yesterday] a tech company with over $10 billion in deposits [payroll, etc.] will get access to $250,000 and an FDIC receiver’s certificate for the rest. The FDIC will pay some ,money in the form of an advance dividend to the certificate holders in a week or two, It won’t be much. It has to come out of the SVB receivership assets.

One of the basic tenets of financial management is diversification of risk. Bank supervisors used to track bank’s concentrations of risk [any holding or sector – here tech start ups – concentration of more than say 50% of capital]. This bank had a huge red flag and it seems no one even saw it.

I bet that cured your iunsomnia.

That face when you realize the FDIC has 30 years to reimburse bank customers 🤯

Home prices are elevated (they are about 45% higher than you’d expect given the change in personal income per household since 2000). However, outstanding household mortgage debt has not increased in real terms over the last 10 years. There’s been an increase in the number of underwater mortgages of late, but the total number still accounts for < 1% of the households in owner-occupied housing.

Household debt service ratios and financial obligation ratios are somewhat below the median of the years since 1979.

P/E ratios in the stock market are mildly elevated – about 14% north of the median of the years since 1971.

Loan delinquency rates at commercial banks are not elevated. There’s been some recent increase in credit card delinquecies, but nothing out of the ordinary.

I’ve never heard of this bank. It has offices in 17 states other than California (three offices in Texas and one in each of the other states). They have four branches in California and a number of other offices therein. As far as I can tell, they do little deposits-and-loans banking. They have ‘private banking’ services and some business banking, but for the most part it seems their clients are established corporations of some size.

One of the basic tenets of financial management is diversification of risk. Bank supervisors used to track bank’s concentrations of risk [any holding or sector – here tech start ups – concentration of more than say 50% of capital]. This bank had a huge red flag and it seems no one even saw it.

I cannot help but wonder how politicized is financial regulation right now. All the debanking of regime opponents (e.g. Gen. Flynn’s wife) doesn’t strike me as something a commercial business would do if there weren’t government officials leaning on them.

As far as I can tell, they do little deposits-and-loans banking. They have ‘private banking’ services and some business banking, but for the most part it seems their clients are established corporations of some size.

I mean little deposits-and-loan banking for households and small businesses.

Art,

I know the Federal bank agencies were in on Obama’s schemes to debank gun manufacturers and retailers.

Contrary to my overlong comment above. This may be a canary in the coal mine for a systemic financial crisis.

If that bank’s main unsafe and unsound conditions were based on now-depreciated bonds [long term debt securities assets] bought when rates were near zero, those unsafe conditions – negative net interest margin – likely exist in many financial institutions. When rates go up, long term bond market values go down. In the past year FF rates went from near zero to 4.75%, the 30-year mortgage went from about 3% to 6.62% [and that’s down from 7%+].

For all this we thank Brandon’s handlers and the Fed.

About 26% of the assets of commercial banks in this country are in the form of securities. I’m looking at some sites on bond prices and it appears that trading 5-10% below par value is common right now.

This was entirely caused by Trump, climate change, racism, and intolerance. Anyone who says otherwise is a CO2 emitting MAGA racist.

We likely will never learn what really happened. You can’t handle the TRUTH.

See the 4Q2022 FFIEC Call Report: Securities – $117.3B, 56% [very high] of Total Assets; Loans – $73.6B, 35% [very low] of TA; Cash and equivalents – $12.5B – 6% [a bit high] of TA but not enough to meet $42B of withdrawals.

Seems SVB had to sell deeply [market price] depreciated [rates rise securities market prices fall] securities to cover withdrawal demands. The Fed kept rates near zero way too long. Then [better late than never], since March 2022 the FF effective rate is up from 0.09% year ago to 4.58%, the 30-year mortgage rate from about 3% to around 6.6%.

See Fed FOMC rate increases and Fed balance sheet shrinkage.

Fed kept market interest rates at near-zero far too long – Is there systemic disaster from a possible huge overhang of deeply depreciated bonds on banks’ books?

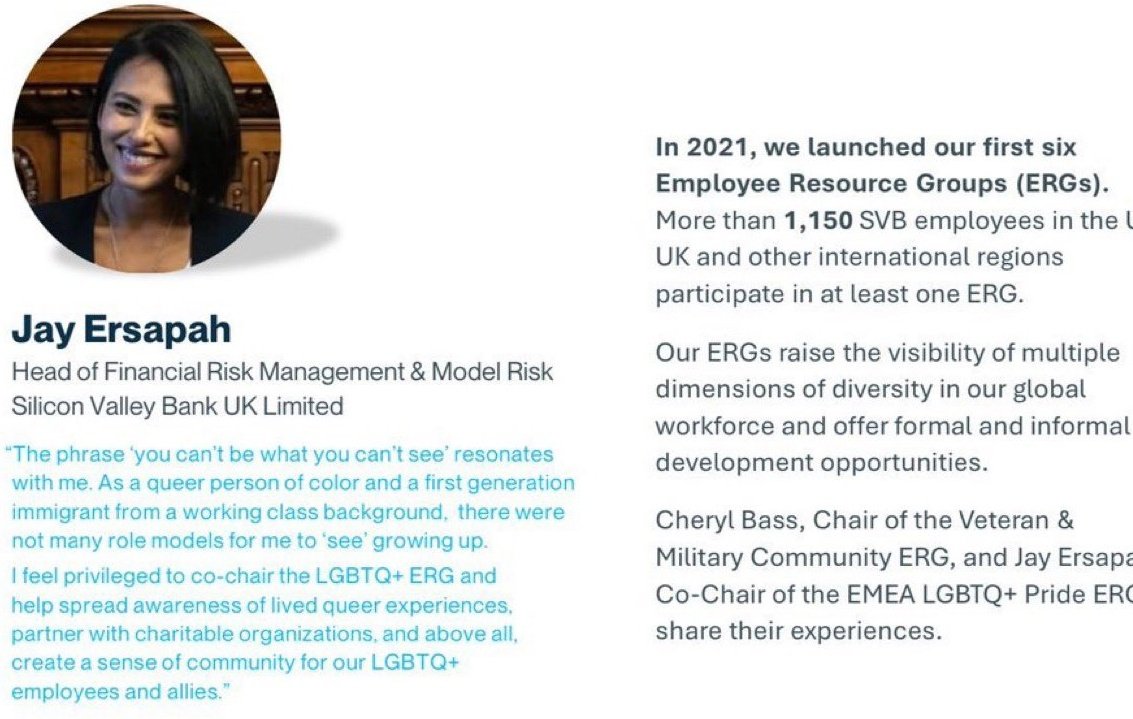

https://www.dailymail.co.uk/news/article-11848705/Woke-head-risk-assessment-Silicon-Valley-Bank-accused-prioritizing-diversity-issues.html

This is the head of risk management for their British subsidiary. (Who has now deleted her LinkedIn profile). Elites in every sector are devoted to their performative games in lieu of actually doing their jobs. How did this happen?

Former Comptroller of the Currency under Trump, Keith Noreika, had an interesting observation yesterday (3/11/23) @ Semafor . com: “The FDIC and the Fed had the chance to save the bank by allowing it to merge or by finding a buyer for it, as they’re allowed to do so by law. Had they done so, no depositor would be at risk. Instead due to strong merger approval opposition from the far left, they hesitated. Now they are faced with the possibility of a full bailout.”

The acting Comptroller of the Currency is a Biden appointee, Michael Hsu, since May, 2021: if you go to the Comptroller/Currency website, one of Hsu’s most recent focuses was, on March 1st, an address celebrating the Carter Admin-era 1977 Community Reinvestment Act, an early and rightly controversial forerunner of ESG and DEI, which has often resulted in pouring money into loser (and sometimes fraudulent) political entity “communities of color” boondoggle investments. Obviously, Hsu was not watching the inversion of community bank securities (earning about 1.5%), leading to capital flight to safer Fed T-bills earning now about 5%-5.5% (due to Jerome Powell’s full gonzo attack on inflation to try to save the Biden admin in 2024).

The Epoch Times is reporting today (Sunday) that Janet Yellin has come out of hiding in the hall bathroom and announced the Fed will not do a full bailout of SVB—but it sounded as if perhaps they (Fed Reserve Chairs) will allow another bank to buy out SVB—a little late—but if so that would be for 60-80 cents on the dollar for uninsured deposit amounts, according to some sources.

Billionaire hedge fund investor Bill Ackman is out warning that the Fed must move quickly, because the next two days (Monday & Tuesday), when markets open, could be crucial, and the Fed may not be able to reverse bank runs on other community banks which also have large uninsured deposit balances. SVB’s uninsured deposits ranged from about 89% as T. Shaw points out, to as high as 95%. There are at least 11 other mid-size banks that are in this category of highly exposed institutions.

Steve,

Latest and Greatest.

Systemic Risk Averted.

Fed Bailouts: Collateral for Bank Term Funding Program rescue loans will be valued at par, not market value – [editorial] Fairy Tale Value.

“. . . the Federal Reserve Board on Sunday announced it will make available additional funding to eligible depository institutions to help assure banks have the ability to meet the needs of all their depositors. This action will bolster the capacity of the banking system to safeguard deposits and ensure the ongoing provision of money and credit to the economy.”

Adding that all depositors both at [failed] Signature Bank, and also at Silicon Valley Bank, will have access to their money on Monday.

The financing will be made available through the creation of a new Bank Term Funding Program (BTFP), offering loans of up to one year in length to banks, savings associations, credit unions, and other eligible depository institutions pledging U.S. Treasuries, agency debt and mortgage-backed securities, and other qualifying assets as collateral. These assets will be valued at par. The BTFP will be an additional source of liquidity against high-quality securities, eliminating an institution’s need to quickly sell those securities in times of stress.

Stock futures are rising.

@T Shaw.

Thank you. Interesting times we live in.

Also: for most of the past year, SVB, did not have a risk, a risk assessment chief risk officer. The new CRO was just appointed sometime in January, 2023. Only having about 4–6 weeks to fix things is an impossible task. To me, it all comes back to the fact that, as Larry Kudlow, Arthur Laffer, Steve Forbes, and Rand Paul have warned, Jerome Powell’s monomaniacal focus on rapidly raising the Fed prime interest rate to “battle inflation” will have unintended potentially catastrophic outcomes.

I’m not understanding why no legal provision was ever made for the FDIC to re-capitalize the bank by dispossessing the shareholders and swapping the outstanding bond debt for equities. If that wasn’t enough, they could swap the outstanding bond debt and the outstanding commercial paper for equities. If that wasn’t enough, the outstanding bond debt, the outstanding commercial paper and some portion of the uninsured deposits. Replace the top management with trustees, clawback the bonuses distributed on the eve of failure, and prosecute the CEO and CFO for insider trading.

Billionaire hedge fund investor Bill Ackman is out warning that the Fed must move quickly,

Bet he’s talking book.

Jerome Powell’s monomaniacal focus on rapidly raising the Fed prime interest rate to “battle inflation” will have unintended potentially catastrophic outcomes.

I hope Powell stays the course.

I was thinking the FOMC would not raise rates this week, but the powers that be did the above and maybe they’ll go up 25 bp.

Powell’s mistake was not beginning slowly to raise rates in March 2021 – transitory, supply chain constipation, Putin – the same month Biden’s handlers pushed in the economy $1.9 trillion in printed money. So, in March 2022, the first moth FOMC raised the Fed Funds target 25 basis points, the effective FF rate was 0.09% and CPI rise was 8.5% year-on-year, 1.2% month-on-month. Now, the effective FF rate is 4.58% and CPI rose latest report we have 6.4% YoY and 0.5% MoM.

Historic note FF target rates were 0.0% – 0.25% from January 2009 to December 2015 up 25 bp that month and four rate increases in 2018, then returned to 0% – 0.25% from March 2020 to March 2022. Concomitantly, to suppress long rates, the Fed purchased trillions in long debt securities called it ‘quantitative easing.’

With a brief interruption in 2018 rate increases FF target rates were 0% – 0.25% from January 2009 to March 2022. And in thgat interval massive Fed QE purchases kept long term rates unnaturally low. Last year the 30 year fixed mortgage rate was 3% now it’s 6.62%.

They persist [bail outs, controls, financial engineering, interferences, politics, regulations] in refusing to allow markets to clear. Then they blame markets for financial crises.