Donald R. McClarey

Cradle Catholic. Active in the pro-life movement since 1973. Father of three, one in Heaven, and happily married for 43 years. Small town lawyer and amateur historian. Former president of the board of directors of the local crisis pregnancy center for a decade.

My son has $70,000 in grad school debt. He has a plan to pay it off in seven years. Made an Excel spreadsheet-amortization table and everything.

His father is pleased as punch about the spreadsheet.

They must be in why we had to sign 20 papers saying we understood we had to pay back ….i almost left on 19th

He clearly rolled the loan over and consolidated it and usury rates. That’s the only way you end up with a loan that’s steeper than a mortgage. He probably also had a lousy credit rating, loans on a bunch of other things and this wasn’t his priority.

THIS is why the university system forces you take “higher math” and discourages business math!!

I had almost as much debt when I graduated from law school as this clown and his wife combined. That was over 44 years ago. I paid them all off within 12 years with no defaults, while paying a mortgage and an auto loan for most of that period. As BillR noted, this guy must have been playing games with his loans. No way does it take that long if you pay on time every month, as you promised you would do. I suspect we are not hearing the whole story from “socialist steve.”

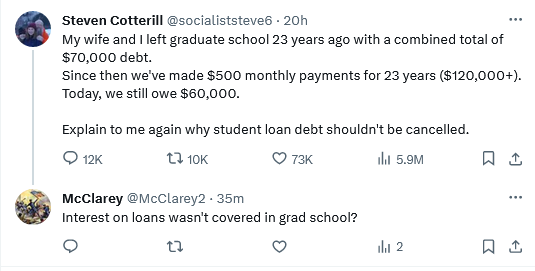

They have a few different plans you can take. The standard 10 year plan and an IDR plan are the most common.

Sounds like he took an IDR plan and failed to read the fine print about interest and principal payments.

Reminds me or a YouTube clip I saw sometime back of a guy at the end of his car lease discovering that he didn’t actually own the car at the end of the term. This could be his brother LOL

He hasn’t said much on Twitter the last four years. His 2019 posts are repellent. His LinkedIn indicates he is employed by the Loudon County, Va. school system. Apparently, one of his side gigs is teaching jail inmates. I’d be more impressed if he didn’t fancy they’re in jail ‘because they are poor’. He is 58 years old per some sources. He and his wife apparently have two daughters, who look rather young to have a father in his age range.

I’ve found an address associated with his name. It’s in Charles Town West Virginia, an exurb of DC, about 60 miles out from K Street, 30 miles from the population center of Loudon County. Redfin and Zillow put the value of his house at somewhere between $330,000 and $370,000. It has 2,800 sq feet of interior space, three bedrooms, and 1.5 baths.

There’s something wrong with the story.

Cotterill claims he and his wife have made $500/mo monthly payments on an original borrowed principal of $70k? He alleges $500/month? Every month, timely payments? And yet he has a principal balance left of $60k? Sorry, that doesn’t make mathematical sense.

If he borrowed the money around year 2000-2001 (“23 years ago” he says), the historic interest rates (based annually on the 10-year treasury bill auction in May) at that time ranged between about approx. 5.39% and 8.19%. (“ Historical Federal Student Loan Interest Rates and Fees,” Savingforcollege.com). Even if his loan was at the max rate of 8.2% at that time, he should’ve wanted to pay about $677 per month and he would’ve paid it off in 15 years. The total amount of interest he would’ve had to pay would have been $51,871 in addition to the $70k principal.

Cotterill underpaid by about $177/mo what should have been paid if he wanted to amortize the loan in, say, 15 years. At the rate that he’s paying, is going to take him well over 30 perhaps almost 40 years. That’s on him.

But he claims he has a $60K principal remaining after 23 years?

Even if he underpays what he should’ve been paying per month, his principal after 23 years @8.2% should now be about $33,500 —not $60,000. So that part of the story doesn’t make sense at all.

The Federal government required banks to provide amortization schedules (US banks were doing the direct lending at that time in programs overseen by the US federal government), telling the student how much they needed to pay monthly. He had to have seen in his monthly statement that he was in negative amortization and not paying the full amount of interest due monthly on his monthly statement.

And there were advantageous periods subsequently that he could’ve refinanced that loan at a lower rate—sometimes as low as 3-4%. Why didn’t he do so?

I know this is a lot of “green eyeshade” stuff for most people —-but his story doesn’t mathematically calculate at all.

@ Bill R: spot on. He had to have rolled the original loan over and either added debt or he wasn’t paying timely even at $500 a month.

Or something. His story doesn’t check out. (that’s the thing with numbers. They always bite left leaning Democrats in the arse.)

Aren’t student loans a way to subsidize the College-Industrial complex? The principal money ends up in the college bank accounts with little incentive to moderate ever escalating tuitions. There is no cash surrender value to a college degree, the student is always underwater and upside down on the loans. There is no equity position or physical asset like a car or a house that can be repossessed.